This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Regulators seeking ways to balance protection of customers’ interests, financial institutions’ risks, and their other policy objectives for digital banking can learn from early regulatory experiences.

Blockchain technology promises to transform banking, financial services, and FinTechs by enhancing the digital customer experience while lowering costs and reducing data risks in a secure environment. In recent years, blockchain adoption has increased in banking and financial services and the emerging FinTech industry.

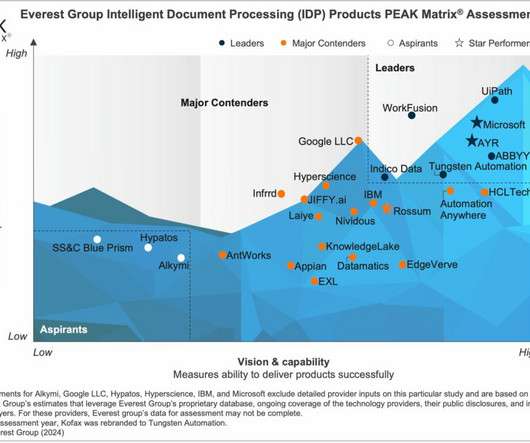

Intelligent Document Processing (IDP), Banking-specific IDP, and Insurance-specific IDP Products Intelligent Document Processing (IDP) products continue to play a vital role in enterprises’ automation technology portfolios. Advances in generative AI are driving providers to ramp up their IDP capabilities.

Webinar Realize your Embedded Finance and Lifestyle Banking strategy November 16, 2023 8:00 AM PT | 11 AM ET Join Everest Group Practice Director Kriti Seth in this upcoming webinar to discover how innovative platforms empower financial institutions to navigate the evolving banking regulatory landscape and revolutionize customer experiences.

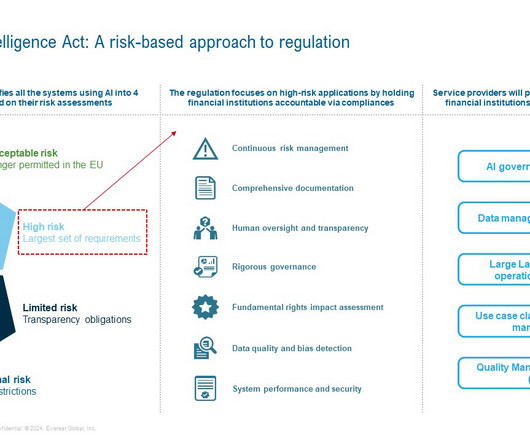

Artificial intelligence (AI) is poised to affect every aspect of the world economy and play a significant role in the global financial system, leading financial regulators around the world to take various steps to address the impact of AI on their areas of responsibility.

Open banking – a system that provides third-party access to financial data through application programming interfaces (APIs) – has unlocked digital financial innovation and disruption. Read on for more on our latest open banking research. . Read on for more on our latest open banking research. .

As US regulators consider a decision on open banking, account-to-account (A2A) payments face challenges in a card-dominated market but also have some promising use cases.

This deal holds the potential to significantly impact the banking and financial services (BFS) IT services market and providers. If the Capital One merger clears antitrust regulations, the combined entity would become the sixth-largest US bank by assets and a leading card issuer and network provider for the US payments market.

This blog post delves into the pivotal role these practices play in ensuring the stability and success of financial institutions and banks. Legal Obligations and Regulatory Frameworks It is well-known that financial institutions operate within a complex web of laws and regulations. The Role of Regulatory Risk and Compliance 1.

In APAC, vast political, economic, and social differences among countries pose an impact on sustainable finance regulations. Even for ESG factors that are easiest to measure and compare — carbon emission, for example — there are still no common goals in the region.

With Australia facing a looming recession, outsourcing is emerging as a solution for banks and financial institutions to navigate economic uncertainty, improve efficiency, and find expert talent. Will banks suffer? In one word: Yes. Financial services have been significantly impacted by the Australian recession.

This regulation will have an impact on both crypto users and providers. In fact that raises a number of unanswered questions among regulators regarding appropriate regulatory measures. LinkedIn The post Crypto Compliance – the new EU regulation appeared first on Infosys Consulting - One hub. Many perspectives.

With the recent banking implosion, the global financial services industry , technology companies, and service providers will be hit in different ways. Let’s explore the reverberations of these concerning banking trends. We believe this will start a domino effect impacting bankingregulations, profitability, and technology spend.

This is primarily due to the unprecedented rise of FinTechs, PayTechs, and neo-banks, which introduce faster, innovative, and convenient transaction methods such as Buy Now Pay Later (BNPL), digital wallets, Request to Pay (R2P), embedded payments, and digital currencies. Today, consumers have more payment options than ever before.

Recognizing that regulated and non-regulated financial institutions seek to engage in cryptocurrency and crypto asset activities, the three largest federal bankregulators, the Federal Reserve, the Federal Deposit Insurance Corporation, and the Office of the Comptroller of the Currency, recently issued a joint statement on crypto assets.

Markets around the world are very different regarding payment preferences, technological and commercial maturity, and regulations. A ‘one-size-fits-all’ approach is inadvisable.

Recently, I attended the 2023 Bank Automation Summit , where one of the significant topics of discussion was how banks navigate their transition to the cloud. The “cloud” refers to a global network of servers, each with a unique function, that works in tandem to enable users to access files stored within from any approved device.

As the region’s regulators increase license allocations and set standards for the next wave of digital banks, there are opportunities for both incumbents and new entrants to enter the arena.

Seeking additional arrows in their quiver against large bank failures, on October 14, 2022, the Federal Reserve Board (FRB) and Federal Deposit Insurance Corporation (FDIC) published an Advance Notice of Proposed Rulemaking (ANPR). Current Category I-III Bank Rules. For large banking organizations that are not U.S.

The retail banking industry is faced with significant challenges to achieve optimal operational efficiency and profitability while providing the highest level of customer satisfaction. Retail banks offer a wide variety of products, including consumer loans, credit cards, and checking and savings accounts. READ REPORT NOW.

Central Bank Digital Currency (CBDC) ). For those wanting to start their own cryptocurrency fund, it’s important to be well informed about cryptocurrency regulations. Regulatory cryptocurrency regulations are most fluid at the state level. State Regulations.

The lines between banks and banking are blurring more and more. Traditional banking and financial services firms have been slow to react. Traditional banking and financial services firms have been slow to react. Successful banking process improvement requires placing equal importance on internal and external forces.

Banks need to evolve International Financial Reporting Standard (IFRS) 9 models quickly—and those that get it right will have more than just a competitive advantage.

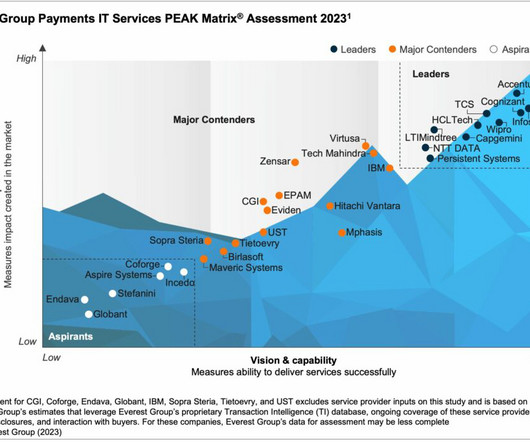

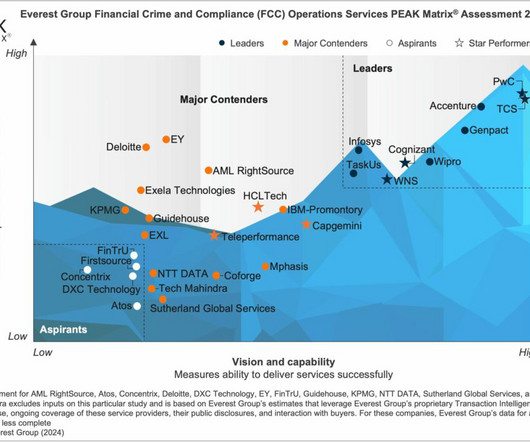

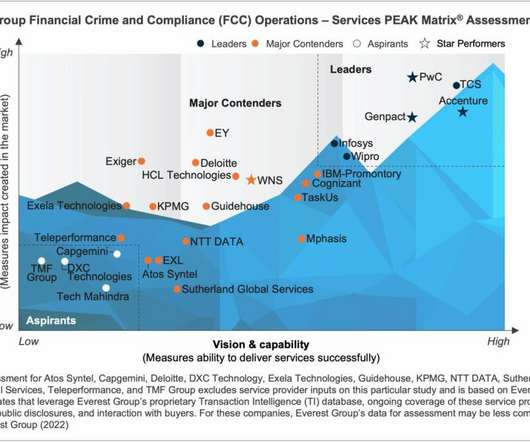

Financial Crime and Compliance (FCC) Operations Services The Financial Crime and Compliance (FCC) operations landscape is rapidly expanding within the Banking and Financial Services (BFS) industry. They are working to safeguard themselves from financial crimes while managing operational costs and enhancing delivery capabilities.

A competent team should demonstrate extensive knowledge of Global Distribution Systems (GDS), Online Travel Agency (OTA) operations, and travel regulations. Plus, these teams often work from locations with lower costs, giving you access to top talent without breaking the bank.

Silicon Valley Bank’s (SVB) collapse is still reverberating around global markets, causing investors to scrutinize the institutions at the heart of the startup ecosystem and prompting plunges in some banks’ stock prices despite the rapid response of bankingregulators worldwide.

intermediate holding companies of foreign banking organizations , and certain insured depository institutions. The proposed eligible LTD requirement was calibrated primarily on the basis of what the proposed regulation refers to as a “capital refill” framework. Comments must be received on or before November 30, 2023.

Recent headlines have highlighted the failure of SVB Financial Group, the parent company of Silicon Valley Bank (“SVB”). We’re putting this into practice and offering our predictions concerning what regulations may arise once the dust has settled. Perhaps capital was not the primary cause of the bank’s failure.

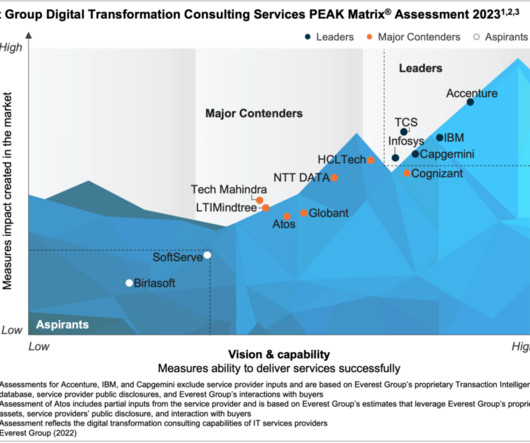

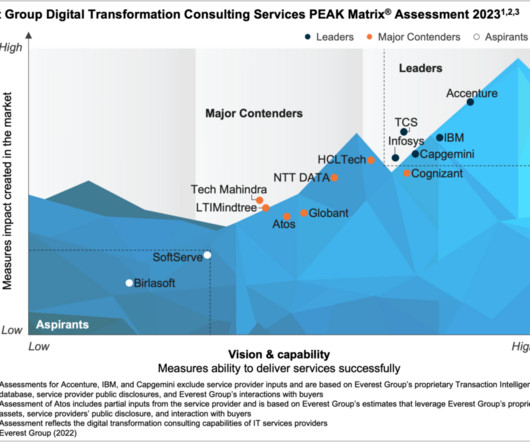

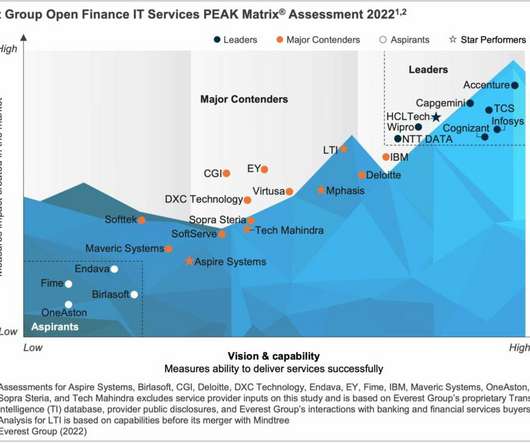

Top Open Finance IT Services The concept of open banking is no longer restricted to payment services. These use cases are giving rise to concepts such as embedded finance, buy now pay later, and super-apps, which will allow banks to deliver hyper-personalized products and become more customer-centric. Learn More. Learn More.

We are witnessing a sea-change in the way data is managed by banks and financial institutions all over the world. Data being commoditized and, in some cases, even monetized by banks is the order of the day. “The Business”, in traditional banks, is treated like a larger-than-life entity that needs to be supported by IT. .

As regulators encourage new players to enter the digital financial services sector, firms that take the initiative can gain an early advantage in one of the world’s largest greenfield markets.

These requirements create a technical challenge for enterprises—especially in regulated industries (e.g., insurance, banking, healthcare, etc.)—to How are IBM Cloud regulated workloads set up and connected to other clouds? Why are regulated workload components spread across multiple clouds?

Gen AI has recently gained considerable attention in the banking, financial services, and insurance (BFSI) industry. Security measures In a highly regulated industry like BFSI, where data and security are imperative, meticulous attention to security and regulatory compliance is critical.

Trust is the cornerstone on which the banking industry is built. When consumers lose trust in a bank’s ability to manage risk, the system stops working. Put simply, consumers trust banks to keep their money safe and return the money when requested. But there’s trust on the business side, too.

While the future of digital assets was once uncertain, the recent surge in investments, partnerships, and pilot use cases spearheaded by banks and technology giants has laid the doubts to rest. This holds particularly true for cryptocurrencies, stablecoins, and Central Bank Digital Currencies (CBDCs).

Moreover, many of these financial services applications support regulated workloads, which require strict levels of security and compliance, including Zero Trust protection of the workloads. To deliver this service, the bank application employs an ecosystem of partner applications interoperating using the BIAN framework. initiative.

Top Financial Crime and Compliance (FCC) Operations Service Providers Financial Crime and Compliance (FCC) operations continue to grow within the Banking and Financial Services (BFS) industry. New regulations in the financial sector call for a dynamic regulatory compliance check, which is difficult for these institutions to manage globally.

The Office of the Comptroller of the Currency (“OCC”) issued a letter (1179) that national banks and federal savings associations must demonstrate that they have adequate controls in place before they can engage in cryptocurrency, distributed ledger, and stablecoin activities.

However, this unprecedented growth has also raised concerns about the potential risks associated with the unchecked use of AI, prompting the need for regulations to ensure the responsible development and deployment of these powerful technologies.

Banks, lenders, FinTechs, and other banking and financial services (BFS) enterprises are expanding into new markets following the rising customer demand. From nearly US$47 billion in 2021, the global neo-banks market is poised to be valued at US$2.05 trillion in 2030, growing at a CAGR of 53.4%

Read on to understand the new global capital market trends, the staying power of retail investors, and the impact on investment banks, asset and wealth managers, and service providers. The subdued demand was visible in the quarterly earnings results of some major investment banks.

The Banking, Financial Services, and Insurance (BFSI) industry faces various challenges in today’s evolving environment, from inflation and cybersecurity to increased competition from fintechs, and changing customer expectations. Cost effective and pay-as-you consume model through DaaS or VDI Embracing Banking 4.0

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content