This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

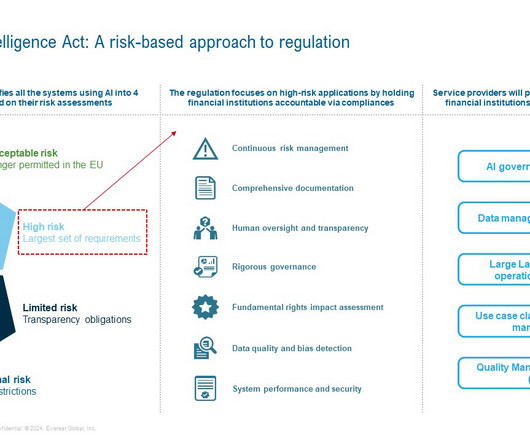

The regulatory paradox: Why AI governance struggles to keep pace As AI advances at breakneck speed, global regulatory efforts are proving insufficient in addressing its environmental and ethical implications. The European Union (EU) AI Act, heralded as a landmark regulation, aims to impose risk-based compliance measures.

Blockchain technology promises to transform banking, financial services, and FinTechs by enhancing the digital customer experience while lowering costs and reducing data risks in a secure environment. In recent years, blockchain adoption has increased in banking and financial services and the emerging FinTech industry.

Artificial intelligence (AI) is poised to affect every aspect of the world economy and play a significant role in the global financial system, leading financial regulators around the world to take various steps to address the impact of AI on their areas of responsibility.

Cloud service providers are vital partners in helping Banking and Financial Services (BFS) institutions build robust systems for cloud migration and exit strategies to maneuver complex regulatory and operational environments. Major banks have spearheaded the charge towards cloud portability by embracing technologies that allow flexibility.

Learn the steps organizations should take to prepare now and discover how the new DORA regulations will strengthen digital operational resilience. The DORA regulations are expected to significantly enhance the digital resiliency of the EU’s financial sector and foster greater stability, consumer protection, and trust.

Open banking – a system that provides third-party access to financial data through application programming interfaces (APIs) – has unlocked digital financial innovation and disruption. Read on for more on our latest open banking research. . Read on for more on our latest open banking research. .

With the recent banking implosion, the global financial services industry , technology companies, and service providers will be hit in different ways. Let’s explore the reverberations of these concerning banking trends. We believe this will start a domino effect impacting bankingregulations, profitability, and technology spend.

With Australia facing a looming recession, outsourcing is emerging as a solution for banks and financial institutions to navigate economic uncertainty, improve efficiency, and find expert talent. Will banks suffer? In one word: Yes. Financial services have been significantly impacted by the Australian recession.

Recognizing that regulated and non-regulated financial institutions seek to engage in cryptocurrency and crypto asset activities, the three largest federal bankregulators, the Federal Reserve, the Federal Deposit Insurance Corporation, and the Office of the Comptroller of the Currency, recently issued a joint statement on crypto assets.

However, this unprecedented growth has also raised concerns about the potential risks associated with the unchecked use of AI, prompting the need for regulations to ensure the responsible development and deployment of these powerful technologies.

by the World Bank – PSEB. The Government offers zero income tax on IT exports till June 2025. The government was keen on collaborating with us as one of the first movers in that geography. The Pakistan government itself collaborated with us on the most favorable tax abatements at the outset.

The lines between banks and banking are blurring more and more. Traditional banking and financial services firms have been slow to react. Traditional banking and financial services firms have been slow to react. Successful banking process improvement requires placing equal importance on internal and external forces.

We are witnessing a sea-change in the way data is managed by banks and financial institutions all over the world. Data being commoditized and, in some cases, even monetized by banks is the order of the day. “The Business”, in traditional banks, is treated like a larger-than-life entity that needs to be supported by IT. .

Similar to GDPR for privacy, the EU AI Act has potential to set the tone for upcoming AI regulations worldwide. The EU AI Act aims to meet the challenge to develop and deploy AI responsibly across industries including those that are highly regulated such as healthcare, finance and energy. million euros or 1.5%

Members of Perficient’s Digital Asset Team have advised followers in multiple online articles about the digital asset revolution and relevant regulations affecting the same in the United States. Central Bank Digital Currency (CBDC) – Perficient Blogs. Central Bank Digital Currency (CBDC) – Perficient Blogs.

Gen AI has recently gained considerable attention in the banking, financial services, and insurance (BFSI) industry. Security measures In a highly regulated industry like BFSI, where data and security are imperative, meticulous attention to security and regulatory compliance is critical.

Any business loan or line of credit from a bank—brick-and-mortar or online—will carry more favorable terms if you have a decent business credit scor e. Lenders use your business credit score to determine how likely you are to repay your loan; the lower the score, the less attractive you are to a lender, especially banks.

Sustainability in insurance transcends traditional practices, weaving Environmental, Social, and Governance (ESG) elements into the core of day-to-day operations, thereby safeguarding the future of stakeholders and the planet. Regulatory changes are also pushing the insurance industry towards greater transparency and sustainability.

Global Business Services (GBS) organizations have a big opportunity to champion Environment, Social, and Governance (ESG) in banking and financial services (BFS) institutions. These organizations are also focusing on workplace diversity , pay equity, and good governance structure to meet their ESG aspirations.

Trust is the cornerstone on which the banking industry is built. When consumers lose trust in a bank’s ability to manage risk, the system stops working. Put simply, consumers trust banks to keep their money safe and return the money when requested. But there’s trust on the business side, too.

Read on to understand the new global capital market trends, the staying power of retail investors, and the impact on investment banks, asset and wealth managers, and service providers. The subdued demand was visible in the quarterly earnings results of some major investment banks.

While the future of digital assets was once uncertain, the recent surge in investments, partnerships, and pilot use cases spearheaded by banks and technology giants has laid the doubts to rest. This holds particularly true for cryptocurrencies, stablecoins, and Central Bank Digital Currencies (CBDCs).

Banks, lenders, FinTechs, and other banking and financial services (BFS) enterprises are expanding into new markets following the rising customer demand. From nearly US$47 billion in 2021, the global neo-banks market is poised to be valued at US$2.05 trillion in 2030, growing at a CAGR of 53.4%

Additionally, the Supervisory Letter states that Board-supervised banking organizations should notify the Board prior to engaging in crypto-asset-related activities. The letter highlighted mandatory compliance with the following federal regulations: The Bank Holding Company Act. The Home Owners’ Loan Act. Financial risk.

Our research highlights the transformative power of technology in reducing carbon footprints, enhancing energy efficiency, and driving sustainable practices across sectors as diverse as oil & gas, banking & finance, and manufacturing. This is a theme prominent not just at an enterprise level, but also at an international level.

The social credit system was designed to make sure individuals and businesses in China comply with the country’s laws and regulations. China’s social credit system gives individuals, businesses, and government entities a credit score based on their trustworthiness. But you might violate regulations without even realizing it.

But you know what, anything that can make more money, intelligently in the long term is a good idea for all investors, investment managers, banks and consultants like me. Governance factors focus on the organization’s leadership, transparency, accountability, and adherence to ethical business practices.”

But you know what, anything that can make more money, intelligently in the long term is a good idea for all investors, investment managers, banks and consultants like me. Governance factors focus on the organization’s leadership, transparency, accountability, and adherence to ethical business practices.”

The Consumer Financial Protection Bureau (CFPB) recently issued a final rule § 1033.121(c) supporting open banking and personal financial data rights. Under this ruling, banks, credit unions, credit card issuers, and other financial service providers must enhance consumer access to personal financial data.

The financial services industry has been in the process of modernizing its data governance for more than a decade. But as we inch closer to global economic downturn, the need for top-notch governance has become increasingly urgent. Regulatory compliance The financial space is highly regulated. How did it get there?

Today, we are seeing significant digital disruption in the business of trade and supply chain financing that is largely influenced by global events and geopolitics, changing regulations, compliance and control requirements, advancements in technology and innovation, and access to capital.

Many banks, credit unions, and credit providers were left asking themselves, “when do we expect this to turn?”. Now that the government programs are nearing an end and foreclosures are initiating in many states, the time to make sure you’re ready for what is to come is now.

Employing both local and foreign workers must comply with the minimum salary established by the Vietnamese government. This cumbersome and time-consuming procedure is restricted by a number of restrictions and regulations regarding the positions that foreigners may hold. Local regulations. Employment agreements. China: USD 341.

Despite the ongoing global pandemic, and according to government-accredited sources in KSA, many foreign companies are lining up to enter the Saudi market in 2021 and beyond. Most foreign companies willing to do business in Saudi Arabia establish a local office to bid on the various government projects currently being tendered.

Financial support by governments, lower interest rates, and limited consumption opportunities have contributed to rising household wealth, generating increased revenues for wealth management companies from more fees and advisory support. The industry is seeing structural changes in ecosystem participants.

Compliance Most educational institutions are subject to specific financial regulations and reporting requirements. Transparency Automated reporting allows stakeholders like government agencies, school boards, and donors to see clear and accurate insights. Simplified adherence to financial regulations and audit management.

Far-reaching regulations like Europe’s GDPR levy steep fines on organizations that fail to safeguard sensitive information. Examples of data privacy laws Compliance with relevant regulations is the foundation of many data privacy efforts. One cannot overstate the importance of data privacy for businesses today.

Additionally, as governments worldwide enforce stricter data protection and security regulations, enterprises face pressure to comply with these regulations and adhere to localized data privacy laws. Examples include Europe’s GDPR, California’s CCPA, and Brazil’s LGPD, reflecting the evolving regulatory landscape.

For businesses dealing in perishable goods — whether it’s a production company or retail business — IoT and automation enable better compliance by ensuring refrigerated food products don’t exceed or go below the FDA regulations on temperature thresholds. The technologies can also restrict or grant privileges for operating specific machinery.

One of the greater concerns, in both the crypto community as well as financial regulators and government, is the value stability of the crypto asset. No one wants a failure of one cryptocoin to cause an electronic bank run that in turn causes the value of other crypto coins to plunge.

Highly regulated industries, such as the financial services industry, are especially interested in generative AI’s capabilities surrounding how it can support ever-transient regulatory and data governance demands.

Regulatory pressure on payments digitization Many countries have embraced payments modernization and introduced initiatives to speed adoption and regulate the landscape. The Australian government is officially phasing out checks by 2030 as part of a wider range of payment reforms for the digital era. billion checks processed that year.

Have we removed personally identifiable information and adhered to all regulations? Can we document and be ready to show regulators or investigators that there is no bias in the data? If data is not processed and made usable and trustworthy while adhering to governance policies, AI and ML models will deliver untrustworthy insights.

In parallel, HR Blizz, our tech-forward, end-to-end global payroll platform covering regulations in over 160 countries, leverages Natural Language Processing (NLP), Machine Learning (ML), and workflow automation to optimize payroll operations. Unlike many in the industry, we do not rely on third-party local vendors for last-mile services.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content