This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

We are witnessing a sea-change in the way data is managed by banks and financial institutions all over the world. Data being commoditized and, in some cases, even monetized by banks is the order of the day. Though this seems to be at a stage where some more push is required in terms of adoption in the riskmanagement function.

With the recent banking implosion, the global financial services industry , technology companies, and service providers will be hit in different ways. Let’s explore the reverberations of these concerning banking trends. We believe this will start a domino effect impacting banking regulations, profitability, and technology spend.

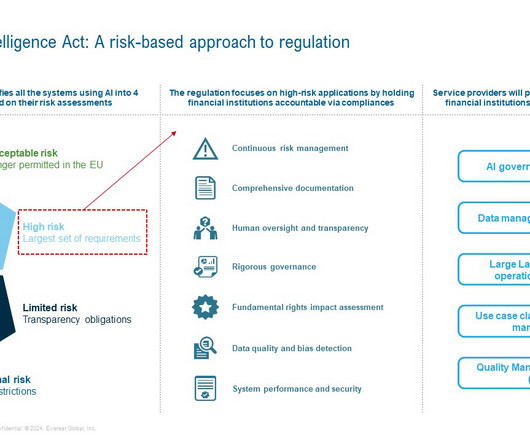

Crucially, a cross-functional team should be formed to oversee AI riskmanagement, drive compliance efforts, and execute mitigation plans across the organization. By taking these steps, enterprises can future-proof their AI initiatives while upholding the standards set forth by the landmark regulation.

The lines between banks and banking are blurring more and more. Traditional banking and financial services firms have been slow to react. Traditional banking and financial services firms have been slow to react. Successful banking process improvement requires placing equal importance on internal and external forces.

Financial institutions’ reliance on information and communication technologies (ICT) for core operations brings immense opportunities in today’s digital world but also exposes banks, investment firms, insurers, and other financial entities to significant cyber threats and operational risks.

Risk Guide is delighted to bring a very special short episode from the very first series of our Extreme Risk Podcast in collaboration with Runderc. For further information about Mykhailo and his career, you can find the RiskManagers Getting Coffee series on: [link]. About the Podcast.

Trust is the cornerstone on which the banking industry is built. When consumers lose trust in a bank’s ability to managerisk, the system stops working. Put simply, consumers trust banks to keep their money safe and return the money when requested. But there’s trust on the business side, too.

” European Parliament News The EU AI Act in brief The primary focus of the EU AI Act is to strengthen regulatory compliance in the areas of riskmanagement, data protection, quality management systems, transparency, human oversight, accuracy, robustness and cyber security.

Sustainability in insurance transcends traditional practices, weaving Environmental, Social, and Governance (ESG) elements into the core of day-to-day operations, thereby safeguarding the future of stakeholders and the planet. While accurately forecasting the future remains a challenge, identifying catalysts for market changes is possible.

SIG University Certified Third-Party RiskManagement Professional (C3PRMP) program graduate William Chanto Castro shares the tricks to overcoming the obstacles to meeting risk regulations and requirements. MAS, 2016, p.9). The C3PRMP program was created by Linda Tuck Chapman, an advisor, educator, author and expert.

Global Business Services (GBS) organizations have a big opportunity to champion Environment, Social, and Governance (ESG) in banking and financial services (BFS) institutions. Capital market firms are embracing green underwriting, while asset and wealth managers are steadily moving toward ESG investing.

By Horst Simon, The Risk Culture Builder. Maybe the time has come to finally take the people side out of RiskManagement—let us change the Basle definition and say Operational Risk is just systems, processes and external events, that is anyway the perception that was followed by most in the world.

Views from Risk Professionals across the world. During the recording of “RiskManagers Getting Coffee” which can be found on YouTube HERE as well as on our website here , a few discussions came up with a recurring theme. One was the question of what makes a great riskmanager. Are there examples?

By anchoring the currency to the relatively stable US dollar, dollarization could bring immediate respite from this inflationary ordeal Fiscal discipline enforcer: Fiscal discipline is paramount, and dollarization would eliminate the central bank’s ability to print pesos and fuel government spending.

Any business loan or line of credit from a bank—brick-and-mortar or online—will carry more favorable terms if you have a decent business credit scor e. Lenders use your business credit score to determine how likely you are to repay your loan; the lower the score, the less attractive you are to a lender, especially banks.

A top-leading bank, grappling with business and regulatory challenges, faced scrutiny after failing the Federal Reserve’s annual stress test. To bolster its capabilities and ensure compliance, the bank sought assistance from Perficient in delivering exceptional project and program management services to tackle their significant hurdles.

Additionally, the Supervisory Letter states that Board-supervised banking organizations should notify the Board prior to engaging in crypto-asset-related activities. The letter highlighted mandatory compliance with the following federal regulations: The Bank Holding Company Act. Financial risk. Legal risk.

Highly regulated industries, such as the financial services industry, are especially interested in generative AI’s capabilities surrounding how it can support ever-transient regulatory and data governance demands.

– These are the exact words (with a couple of expletives, that I cannot quote here) – a senior fund administrator from a large investment firm uttered when we were presenting about environment aware financial riskmanagement. So making a profit while doing good is an idea we all can benefit from.

– These are the exact words (with a couple of expletives, that I cannot quote here) – a senior fund administrator from a large investment firm uttered when we were presenting about environment aware financial riskmanagement. So making a profit while doing good is an idea we all can benefit from.

The Russian military action in Ukraine has already significantly impacted thousands of services jobs in this region, but the potential reverberations to nearshore European countries and the larger global services industry could be far more damaging – making it essential to integrate geopolitical riskmanagement in your decision-making now.

Conduct an internal risk assessment: This can help identify and prioritize assets most impacted by a quantum computer cryptographically, thus exposing the organization to greater risk. Establishing a governance structure with clearly defined roles and responsibilities to adopt PQC effectively is also recommended.

Volumes have been written on the cause of the crisis the world is in, surveys have been done and many fingers are pointing in every direction—a couple of these are pointing straight at us, the Risk Professionals. It is time to renovate riskmanagement. The basic RiskManagement process cycle is one of those.

Lead AI Change Management and Governance: Strong data governance can help address some of the concerns related to source attribution and confidence levels in data and foster trust in Gen AI outcomes. Enable AI : Embarking on AI initiatives demands the expertise of AI experts to define a clear vision and strategy.

The Consumer Financial Protection Bureau (CFPB) recently issued a final rule § 1033.121(c) supporting open banking and personal financial data rights. Under this ruling, banks, credit unions, credit card issuers, and other financial service providers must enhance consumer access to personal financial data.

Fast forward to today, we see the recent banking collapse already casting a haze over the business landscape. We also observed the scope is expanding into adjacent and/or non-traditional areas such as riskmanagement and compliance and environmental, social, and governance (ESG).

By Liz Booth for Commercial Risk. A leading Ukrainian riskmanager has told Commercial Risk Europe about some of the biggest challenges facing his profession as the Russian invasion continues. We had been buying cover for all eventualities and it is now paying off ,” said the riskmanager. “ in the future.

This is evident from emerging regulatory requirements and expectations in UK (Bank of England’s Critical Third-Party regime), Europe (Digital Operational Resilience Act)), Australia (APRA CPS-230 Operational RiskManagement) and Canada (OSFI – Operational Resilience and Operational RiskManagement), etc.

The cloud represents a strategic tool to enable digital transformation for financial institutions As the banking and other regulated industry continues to shift toward a digital-first approach, financial entities are eager to use the benefits of digital disruption. Banks want to tap into these new innovations.

ESG for Banks – How to Elevate the Game to Achieve Key Goals Capgemini 4 May 2022. As two-thirds of the financing must be provided by banks, their role is instrumental in achieving the Goals. The good news is that banks across the globe have now put sustainability at the forefront of their growth mission. Internalize Governance.

Accounting tools offer features designed to make compliance management easier. Transparency Automated reporting allows stakeholders like government agencies, school boards, and donors to see clear and accurate insights. Speeds up routine processes like bank reconciliations and invoice creation, reducing administrative workload.

In the previous two articles in this series, we discussed the disruptions caused by Covid-19 to the payments industry and why banks need to make a significant change in their operations. Modifying and testing ability to submit messages to the corresponding bank and associated settlement processes. ISO 20022 Change management.

have spiked , and the potential for operational risk events caused by people, failed processes, and disrupted systems has increased as a result of greater reliance on virtual working arrangements. In addition, cyber threats (ransomware attacks, phishing, etc.)

Payments (including transaction banking offerings) are at the center of everyday banking. This explosion of digital transactions has also seen a rapid decline in legacy payments in Australian banks, closing hundreds of branches and more than 2200 ATMs. Stay tuned! David Coli. Senior Principal.

The role of data and AI in driving sustainability for banks Satish Weber and Tej Vakta Oct 28, 2024 Facebook Linkedin How cutting-edge tech will shape the future of environmental and social impact in banking In finance, the goal is to go green – now more than ever. What follows are key takeaways from the panel.

It’s clear that banks will need to act quickly to comply with the new regulations. December 2024: Banks of EU and Eurozone countries are required to support receiving SEPA instant payments. Banks, payment institutions (PIs) and electronic money institutions (EMIs) can screen entities and individuals only once a day.

Insurers are also offering joint go-to-market (GTM) products to provide comprehensive cyber riskmanagement solutions to enterprises. This provides an opportunity for service providers to work with carriers to provide such tools and applications to help them assess risks associated with a particular firm.

IBM’s Enterprise Cloud for Regulated Industries Building on our expertise working with enterprise clients in industries such as financial services, government, healthcare and telco, we saw the need for a cloud platform designed with the unique needs of these heavily regulated industries in mind. And our work doesn’t stop there.

These DFS500 amendments signal a crucial shift in the regulatory landscape, emphasizing the imperative for robust governance, riskmanagement, and compliance frameworks across the financial industry.

This blog was co-authored by Perficient Risk and Regulatory CoE Member: Alicia Lawrence The announcement of significant amendments to the New York State Department of Financial Services (NYSDFS) regulations on December 1, 2023, represents a pivotal moment for entities operating within New York’s financial sector.

As the fifth-largest economy in the European Union , the World Bank ranks the Netherlands in the top 40 percent of the easiest countries to do business with globally. Companies can also reduce costs through international growth, as some governments offer incentives for companies to invest. and the UK. The partnership between the U.S.

SIG University Certified Third-Party RiskManagement Professional (C3PRMP) program graduate Senthil Jagadeesan shares how important it is to manage the risk associated with artificial intelligence. It provided practical tips and guidance to tackle today’s challenges from Third-party risks. Background.

Whether you work for a hospital, a university, a tech company or a local government office, choosing a feasible initial implementation for RPA is crucial. RPA government and public sector use cases include: Home care support. Underwriting and riskmanagement. Bank statements and payment checks. Frost and Sullivan$.

This is coming from “reputable” institutions such as JP Morgan, Deutsche Bank and others, although it is also important to remember that these are the same institutions that were very clear in their statements that Bitcoin was a scam only three years ago.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content