This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The European Union (EU) AI Act, heralded as a landmark regulation, aims to impose risk-based compliance measures. The prevailing sentiment was that regulations should be light-touch, in order to avoid stifling competition and innovation. Even where emissions are tracked, regional energy disparities complicate regulation.

The retail industry is facing significant challenges as customer expectations rise, technology advances and competition intensifies. By effectively leveraging these tools, retailers can better meet customer needs and strengthen trust in a competitive landscape. Precisely, POS is the center nerve of your retail business.

Blockchain technology promises to transform banking, financial services, and FinTechs by enhancing the digital customer experience while lowering costs and reducing data risks in a secure environment. In recent years, blockchain adoption has increased in banking and financial services and the emerging FinTech industry.

The retailbanking industry is faced with significant challenges to achieve optimal operational efficiency and profitability while providing the highest level of customer satisfaction. Retailbanks offer a wide variety of products, including consumer loans, credit cards, and checking and savings accounts.

Retail investors are here to stay. As global capital markets face macroeconomic headwinds and a liquidity crunch, retail investors are gaining volume in traditional equity and debt markets as well as emerging alternate investments. The strength of retail investors has been fueled by both demand and supply side factors.

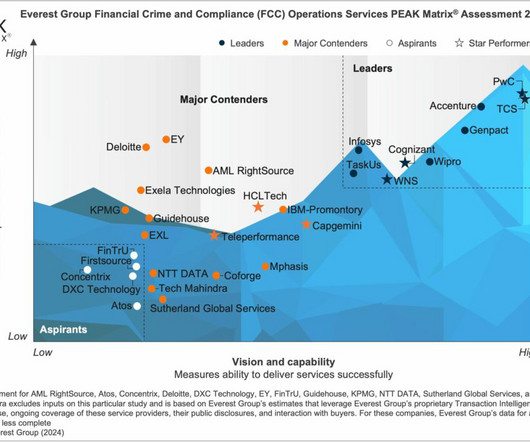

Financial Crime and Compliance (FCC) Operations Services The Financial Crime and Compliance (FCC) operations landscape is rapidly expanding within the Banking and Financial Services (BFS) industry. They are working to safeguard themselves from financial crimes while managing operational costs and enhancing delivery capabilities.

By partnering with IT and technology services providers, banks and financial institutions can prepare for the new T+1 settlement. Read on to understand how this updated regulation will impact the industry landscape and rapidly transform critical areas. The positive impact will vary by the investor type.

While the future of digital assets was once uncertain, the recent surge in investments, partnerships, and pilot use cases spearheaded by banks and technology giants has laid the doubts to rest. This holds particularly true for cryptocurrencies, stablecoins, and Central Bank Digital Currencies (CBDCs).

BPO Philippines Reshaping The Retail & Banking Industry. Retailbanks , like most companies, face an urgent imperative to reimagine themselves. . Consumers’ banking preferences are rapidly evolving. But many banks have yet to fully transition due to limitations of their digital capabilities. .

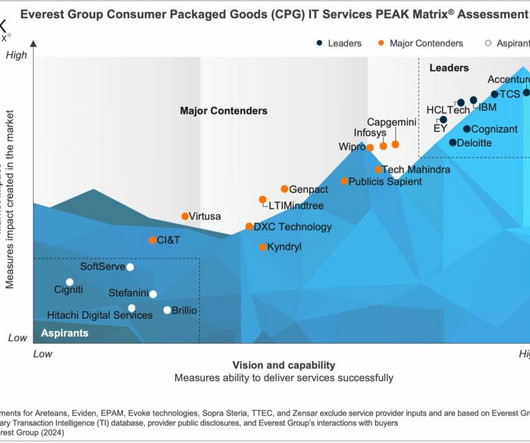

Scope Industry: CPG Geography: global The assessment is based on Everest Group’s annual RFI process for the calendar year 2023, interactions with leading providers, client reference checks, and an ongoing analysis of the CPG IT services market CONSUMER PACKAGED GOODS (CPG) IT SERVICES PEAK MATRIX® ASSESSMENT 2024 Related PEAK Matrix® Assessments PEAK (..)

For instance, when a large bank was infected with ransomware that encrypted the files, the company did not lose much money or experience terrible operational loss because it restored its network from the recent backup. HIPAA regulates the use and disclosure of PHI in the U.S.,

Open Banking is going to do for the banking industry what the introduction of the Apple smart phone did for cell phones. What is Open Banking? Traditionally, banks hoarded financial data, sharing it sparingly on a need-to-know basis.

With shifts in attitudes towards the issue of data ownership illustrated by regulations such as GDPR and concepts such as the open data movement, our guest Huw Davies, Co-founder & Chief Commercial Officer at Ozone API provides his views of financial service platforms implemented through a Banking as a Service-concept.

The Consumer Financial Protection Bureau (CFPB) recently issued a final rule § 1033.121(c) supporting open banking and personal financial data rights. Under this ruling, banks, credit unions, credit card issuers, and other financial service providers must enhance consumer access to personal financial data.

To help shed light on this matter, Perficient’s Financial Services Risk and Regulatory Center of Excellence (CoE) researched the topic extensively and discovered that the Office of the Comptroller of the Currency (OCC) has classified AI as an emerging risk to the banking industry.

Enterprise platform providers such as Salesforce Financial Services Cloud, SAP Digital Manufacturing Cloud, and Oracle Retail Cloud embed industry-specific processes, solutions, and frameworks into their horizontal applications and functions to enable industry specificity. Industry cloud offerings in banking and financial services.

For businesses dealing in perishable goods — whether it’s a production company or retail business — IoT and automation enable better compliance by ensuring refrigerated food products don’t exceed or go below the FDA regulations on temperature thresholds.

Merchants see an increase in revenues, and BNPL is an attractive payment option for consumers due to its lower impact on credit score, increasing regulations on getting a credit card, and a fairer interest rate. Fintechs are surely but steadily eating into the revenue of banks 3 from their consumer lending portfolios.

Buy now, pay later (BNPL) is a type of point-of-sale installment loan that partners with retailers to allow consumers to pay for their purchases in multiple equal payments. When online shopping, if a retailer has a partnership with a BNPL platform, the customer can choose it as their payment method when placing their order at checkout.

In parallel, HR Blizz, our tech-forward, end-to-end global payroll platform covering regulations in over 160 countries, leverages Natural Language Processing (NLP), Machine Learning (ML), and workflow automation to optimize payroll operations. Unlike many in the industry, we do not rely on third-party local vendors for last-mile services.

It eliminates language barriers, allows real-time collaboration in the same time zone, and makes compliance with local laws and regulations easier. Data Protection and Privacy: Ensure compliance with relevant regulations like GDPR, especially when dealing with user data.

An online retailer always gets users’ explicit consent before sharing customer data with its partners. Far-reaching regulations like Europe’s GDPR levy steep fines on organizations that fail to safeguard sensitive information. A navigation app anonymizes activity data before analyzing it for travel trends.

Combined with ongoing supply chain issues, sustainability mandates, evolving regulations, cybersecurity threats and other complexities, industries and enterprises around the world are facing a staggering number of challenges. Together with IBM, CaixaBank, the leading financial group in Spain, worked to transform its omnichannel operations.

Similar to GDPR for privacy, the EU AI Act has potential to set the tone for upcoming AI regulations worldwide. The EU AI Act aims to meet the challenge to develop and deploy AI responsibly across industries including those that are highly regulated such as healthcare, finance and energy. million euros or 1.5%

Retailbanks respond to the Federal Reserve’s short-term interest rate adjustments with corresponding changes in lending and deposit rates. When they need to change direct deposits, clear checks, or open new accounts at a bank, their funds often remain untouched. bank failures but rebounded in the second quarter.

ESG for Banks – How to Elevate the Game to Achieve Key Goals Capgemini 4 May 2022. As two-thirds of the financing must be provided by banks, their role is instrumental in achieving the Goals. The good news is that banks across the globe have now put sustainability at the forefront of their growth mission. COMMITMENT.

Consistent financial reporting is important for several reasons: Transparency : Consistent financial reporting allows stakeholders, such as investors, creditors, and regulators, to have a clear and accurate view of a company’s financial performance over time. Why is Consistent Financial Reporting so Important?

Disability advocacy groups have urged the DOJ to establish regulations to ensure website accessibility for public business entities (e.g., retail stores, banks, hotels, medical facilities, food, and drink establishments and so on). Title III – Businesses Open to the Public.

Unfortunately, the regulations introduced around skilled-migration visas and ANZSCO codes have left some CTOs, CIOs, and other IT decision makers feeling restricted, unable to innovate at the pace nor scale they’d like. Put simply, organisations from retailers to banks to automotive giants are becoming software-first businesses.

This trust extends to meeting both internal compliance mandates and external regulations. Penalties can be substantial, with bank operators receiving seven-figure fines for biased loan eligibility models, and potential GDPR fines of up to 20 million euros or four percent of annual revenue.

It is time to know why banks need to make a significant change in their operations now more than ever. Efficiency – After initiating an international transfer, funds move through multiple correspondent banks before reaching the recipient. Therefore, it has seen a rapid increase in popularity among banks during the pandemic.

Online retailers rely on ASP.NET solutions to develop robust and feature-rich e-commerce platforms that handle a large volume of traffic and transactions. Banks and financial service providers utilize ASP.NET to build secure and scalable online banking systems. ASP.NET has also proven effective in the education sector.

While most carriers have mainly serviced corporate clients, they are now starting to focus on the retail segment by providing standalone cyber insurance products that have typically been sold as add-ons to homeowners insurance.

Verify that the outstaffing company has robust security measures in place, including non-disclosure agreements (NDAs) and compliance with relevant data protection regulations. Data Security and Confidentiality : Protecting your intellectual property and sensitive data is paramount.

How AI is Used in Finance & Banking. Artificial intelligence (AI) plays a critical role in nearly every industry–retail, marketing, manufacturing, healthcare, the list goes on. But we also know that the criteria banks use to make credit decisions aren’t always straightforward or fair.

Financial institutions are part of a heavily regulated sector that still relies to a degree on legacy systems (e.g., A hybrid cloud solution provides a flexible alternative way for banks to isolate this data by hosting applications on industry-compliant public clouds and storing sensitive information on-premises in their private cloud.

In a previous blog post , we discussed how Buy Now Pay Later (BNPL) forces banks to rethink their credit and payment portfolios. This blog will broadly explore what banks need to do to develop a BNPL offer and take it to market. We also touched upon the basic tenets that are essential to consider before embarking on the BNPL journey.

This process helps you understand the equity impact on the company’s financial health and aligns with accounting regulations, which can be further enhanced by leveraging technology and business intelligence solutions for better accuracy. Retail Giants Plc Q4 2022 -$0.8M Retail Giants Plc faced a $0.8M Q2 2022 -$1.5M

Promote cross- and up-selling Recommendation engines use consumer behavior data and AI algorithms to help discover data trends to be used in the development of more effective up-selling and cross-selling strategies, resulting in more useful add-on recommendations for customers during checkout for online retailers.

Retail: Customers can manage their entire shopping experience online—from placing orders to handling shipping, changes, cancellations, returns and even accessing customer support—all without human interaction. This will likely lead to increased regulation and the development of ethical guidelines for AI development and use.

As the fifth-largest economy in the European Union , the World Bank ranks the Netherlands in the top 40 percent of the easiest countries to do business with globally. The most significant sectors in Belgium include public administration, defense, education, health and social work, wholesale retail and food services, and industry.

Asia-Pacific’s software development market is steadily growing due to strict regulations and more business processes requiring applications. The key growth drivers are end users in the finance, banking, online retail and e-commerce, information technology (IT), and healthcare sectors. million in 2013. million in 2013.

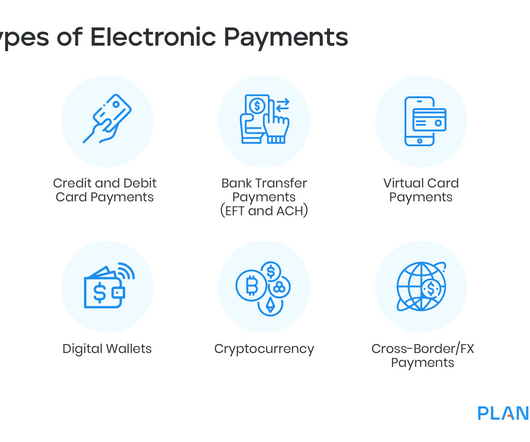

Types of Electronic Payments Common types of electronic payments include credit and debit cards, mobile payment apps such as Apple Pay and Google Pay, online banking transfers, cryptocurrency (Bitcoin, Litecoin etc.), While some payment options require the user to have a formal bank account with a financial institution, others do not.

challenger banks) and B2B (e.g. open banking) products finding room to grow. Many are now well-known brands, like OakNorth Bank, Revolut, Starling Bank, Checkout.com, and Monzo. What are the regulations for fintech? A clear example of this is in Open Banking. The origin of fintech in the UK.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content