This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

We are witnessing a sea-change in the way data is managed by banks and financial institutions all over the world. Data being commoditized and, in some cases, even monetized by banks is the order of the day. Though this seems to be at a stage where some more push is required in terms of adoption in the riskmanagement function.

Learn the steps organizations should take to prepare now and discover how the new DORA regulations will strengthen digital operational resilience. The DORA regulations are expected to significantly enhance the digital resiliency of the EU’s financial sector and foster greater stability, consumer protection, and trust.

Artificial intelligence (AI) is poised to affect every aspect of the world economy and play a significant role in the global financial system, leading financial regulators around the world to take various steps to address the impact of AI on their areas of responsibility.

This deal holds the potential to significantly impact the banking and financial services (BFS) IT services market and providers. Read on to learn the looming risks and what to pay attention to. However, S&P predicts regional and community banks will be interested in mergers of equals this year.

With the recent banking implosion, the global financial services industry , technology companies, and service providers will be hit in different ways. Let’s explore the reverberations of these concerning banking trends. We believe this will start a domino effect impacting bankingregulations, profitability, and technology spend.

This regulation will have an impact on both crypto users and providers. In fact that raises a number of unanswered questions among regulators regarding appropriate regulatory measures. BaFin assumes that payment and value asset service providers are increasingly exposed to money laundering risks. Many perspectives.

However, this unprecedented growth has also raised concerns about the potential risks associated with the unchecked use of AI, prompting the need for regulations to ensure the responsible development and deployment of these powerful technologies.

By partnering with IT and technology services providers, banks and financial institutions can prepare for the new T+1 settlement. This security trade rule change to shorten the order finalization date by a day is expected to enhance operational efficiencies and reduce risk.

The lines between banks and banking are blurring more and more. Traditional banking and financial services firms have been slow to react. Traditional banking and financial services firms have been slow to react. Successful banking process improvement requires placing equal importance on internal and external forces.

Central Bank Digital Currency (CBDC) ). For those wanting to start their own cryptocurrency fund, it’s important to be well informed about cryptocurrency regulations. Regulatory cryptocurrency regulations are most fluid at the state level. State Regulations.

Sir Howard Davies discusses the ways regulations, interest rates, monetary policy, climate risk, and economic threats are affecting the resilience of the banking system.

SIG University Certified Third-Party RiskManagement Professional (C3PRMP) program graduate William Chanto Castro shares the tricks to overcoming the obstacles to meeting riskregulations and requirements. 9). The information required by the Regulator may come from different sources depending on the company.

By Horst Simon, The Risk Culture Builder. Bankregulators have been on a “capital charge”-path for a very long time. No capital charge can be a buffer for bad management of risk. History showed us that sometimes ALL the capital is not enough to save the bank from a risk event gone wrong.

Banks need to evolve International Financial Reporting Standard (IFRS) 9 models quickly—and those that get it right will have more than just a competitive advantage.

In the first half of 2023, there were over 1,715 adjustments to the US state insurance regulations, many of which address climate issues. A notable example is the California Climate Risk Disclosure Survey, which requires insurers to disclose how they are managing climate-related risks.

These requirements create a technical challenge for enterprises—especially in regulated industries (e.g., insurance, banking, healthcare, etc.)—to How are IBM Cloud regulated workloads set up and connected to other clouds? Why are regulated workload components spread across multiple clouds?

Trust is the cornerstone on which the banking industry is built. When consumers lose trust in a bank’s ability to managerisk, the system stops working. Put simply, consumers trust banks to keep their money safe and return the money when requested. But there’s trust on the business side, too.

Any business loan or line of credit from a bank—brick-and-mortar or online—will carry more favorable terms if you have a decent business credit scor e. Lenders use your business credit score to determine how likely you are to repay your loan; the lower the score, the less attractive you are to a lender, especially banks.

By Horst Simon, The Risk Culture Builder. Maybe the time has come to finally take the people side out of RiskManagement—let us change the Basle definition and say Operational Risk is just systems, processes and external events, that is anyway the perception that was followed by most in the world.

Global Business Services (GBS) organizations have a big opportunity to champion Environment, Social, and Governance (ESG) in banking and financial services (BFS) institutions. Capital market firms are embracing green underwriting, while asset and wealth managers are steadily moving toward ESG investing.

Additionally, the Supervisory Letter states that Board-supervised banking organizations should notify the Board prior to engaging in crypto-asset-related activities. The letter highlighted mandatory compliance with the following federal regulations: The Bank Holding Company Act. Financial risk. Legal risk.

Watch the webinar, Transforming to Thrive: Building Winning Operating Models Amid Disruption Across Industries , to learn about trends impacting enterprises across industries, such as healthcare, life sciences, insurance, and banking and financial services?

Automated testing continuously verifies encryption, access controls, and data handling, ensuring that retailers comply with data protection regulations such as PCI DSS. Ensuring data security while complying with regulations like GDPR or industry-specific standards is a critical testing focus.

Highly regulated industries, such as the financial services industry, are especially interested in generative AI’s capabilities surrounding how it can support ever-transient regulatory and data governance demands.

Perficient provides riskmanagement to more than 500 financial services organizations, many of whom have multiple bankregulators. Often an organization will have a state-charted non-member bank, which has the FDIC as its primary federal regulator. The complete 60+ page guidance is available to readers here.

Our bankingrisk and regulatory experts are excited to attend the upcoming XLoD Global event in New York on June 11th. The world’s leading financial institutions and regulators come together at XLoD to discuss the future of non-financial risk and control. What is XLoD Global?

While the world tried to recover from the slowdown, a new predicament posed as a challenge to the Banking industry – new-age Fintech firms. The steady and quick rise of Fintech firms in the world has shaken the presence and role of conventional banking. Banks collaborating and creating partnerships with Fintech is the way forward.

To help shed light on this matter, Perficient’s Financial Services Risk and Regulatory Center of Excellence (CoE) researched the topic extensively and discovered that the Office of the Comptroller of the Currency (OCC) has classified AI as an emerging risk to the banking industry.

Airline, hospital, banking operation, auto company systems and more were crippled across the globe. While it might not be possible to plan for every outage, by ensuring compliance with regulations, enterprises can protect themselves and be in compliance with local laws.

Open Banking is going to do for the banking industry what the introduction of the Apple smart phone did for cell phones. What is Open Banking? Traditionally, banks hoarded financial data, sharing it sparingly on a need-to-know basis.

1] Managing complex business operations across a hybrid multicloud environment presents leaders with unique challenges, not least of which are cyberthreats that can bring essential business functions to a halt—potentially for days, weeks or months. The cost of a data breach at organizations with high levels of noncompliance is 12.6%

Background On Friday, July 28, Heartland Tri-State Bank of Elkhart became the fourth U.S. bank to fail this year. A rather small bank, as of the end of its first quarter, the bank reported $139 million in total assets and $130 million in total deposits in its FDIC Call Report. He was promoted to President and CEO in 2008.

The Consumer Financial Protection Bureau (CFPB) recently issued a final rule § 1033.121(c) supporting open banking and personal financial data rights. Under this ruling, banks, credit unions, credit card issuers, and other financial service providers must enhance consumer access to personal financial data.

Volumes have been written on the cause of the crisis the world is in, surveys have been done and many fingers are pointing in every direction—a couple of these are pointing straight at us, the Risk Professionals. It is time to renovate riskmanagement. The basic RiskManagement process cycle is one of those.

For highly regulated industries, these challenges take on an entirely new level of expectation as they navigate evolving regulatory landscape and manage requirements for privacy, resiliency, cybersecurity, data sovereignty and more. Similarly, in the U.S. Similarly, in the U.S.

For instance, when a large bank was infected with ransomware that encrypted the files, the company did not lose much money or experience terrible operational loss because it restored its network from the recent backup. HIPAA regulates the use and disclosure of PHI in the U.S.,

The payments ecosystem is at an inflection point for transformation, especially as we see the rise of disruptive digital entrants who are introducing new payment methods, such as cryptocurrency and central bank digital currencies (CDBC). This is just one of many examples that show how the payments space has evolved.

The software helps with: Financial Management The software uses detailed tracking and automated processes to ensure that every dollar received and spent is accounted for accurately. Compliance Most educational institutions are subject to specific financial regulations and reporting requirements. You must book a demo to learn more.

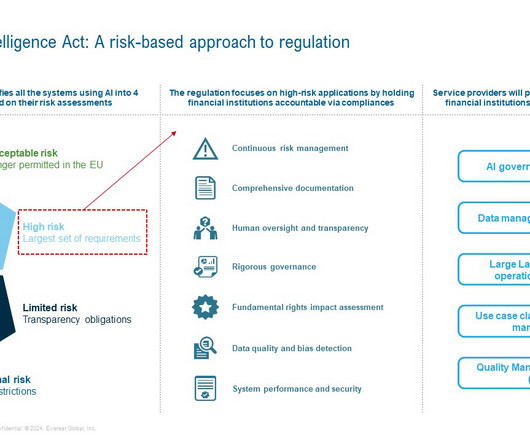

Similar to GDPR for privacy, the EU AI Act has potential to set the tone for upcoming AI regulations worldwide. The EU AI Act aims to meet the challenge to develop and deploy AI responsibly across industries including those that are highly regulated such as healthcare, finance and energy. million euros or 1.5%

A supplier information management portal, for example, can be a “ central source of truth ” for third party relationships and provide all stakeholders with critical information. Consider the General Data Protection Regulation (GDPR) or blockchain technologies. Before joining A.T.

One of the biggest challenges these organizations face is evolving regulations related to payments. To modernize, remain competitive and be compliant with regulations requires organizations to work with a “trusted” technology partner who can help to bring together their traditional payment practices and innovative solutions.

billion of the total cost incurred from the failures of Silicon Valley Bank (SVB) and Signature Bank was designated for safeguarding uninsured depositors. Despite this proactive approach, federal bankingregulators either neglected to review the same documents or did so without taking necessary action before the bank failed.

The cloud represents a strategic tool to enable digital transformation for financial institutions As the banking and other regulated industry continues to shift toward a digital-first approach, financial entities are eager to use the benefits of digital disruption. Banks want to tap into these new innovations.

– These are the exact words (with a couple of expletives, that I cannot quote here) – a senior fund administrator from a large investment firm uttered when we were presenting about environment aware financial riskmanagement. I can assure you, it’s going to impact you if you are an Investor, or a Bank or a Financial Consultant.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content