This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Cloud-based computing will provide tangible benefits for bankingriskmanagement functions, but risk leaders face significant challenges migrating their systems and activities from on-premises to the cloud.

We are witnessing a sea-change in the way data is managed by banks and financial institutions all over the world. Data being commoditized and, in some cases, even monetized by banks is the order of the day. Though this seems to be at a stage where some more push is required in terms of adoption in the riskmanagement function.

The sooner banks start their journey and establish an effective approach to model riskmanagement of cybersecurity solutions, the quicker they will be able to managerisk and establish controls.

With the recent banking implosion, the global financial services industry , technology companies, and service providers will be hit in different ways. Let’s explore the reverberations of these concerning banking trends. We believe this will start a domino effect impacting banking regulations, profitability, and technology spend.

This deal holds the potential to significantly impact the banking and financial services (BFS) IT services market and providers. Read on to learn the looming risks and what to pay attention to. However, S&P predicts regional and community banks will be interested in mergers of equals this year. Capital One’s planned US$35.3

What does it mean for the banking and financial services industry? Beyond trading, agentic AI could enhance riskmanagement by autonomously identifying potential market disruptions or regulatory changes and adjusting exposure accordingly.

If banks reimagine and modernize their business-lending processes, they can take advantage of new opportunities with SMEs and capture more of the forecast growth.

In both the European Union and globally, the new supervisory expectations for credit spread risk in the banking book pose a clear challenge for bank treasury and risk functions.

What to expect from the wegginar: Gain knowledge of exchange rates Recognize the main causes of FX volatility Learn how to invoice your client in their local currency Increase your margins by paying or selling in local currencies Understand your FX riskmanagement options To learn more and to register (n/c), visit: [link].

By partnering with IT and technology services providers, banks and financial institutions can prepare for the new T+1 settlement. This security trade rule change to shorten the order finalization date by a day is expected to enhance operational efficiencies and reduce risk.

Is no news that the banking and finance industry ae facing some constant needs to adapt and continue to offer modern solutions. Staying ahead of the curve is crucial for banks and financial institutions to remain competitive, as clients, rightfully so, don’t forgive bad experiences, especially in terms of their money.

By focusing on six key areas, banks can more accurately manage rising interest rates and credit spread risk across business lines, meet regulatory demands, and create competitive advantage.

The lines between banks and banking are blurring more and more. Traditional banking and financial services firms have been slow to react. Traditional banking and financial services firms have been slow to react. Successful banking process improvement requires placing equal importance on internal and external forces.

Organizations this year plan to enhance their MRM framework capabilities—including risk culture, standards, and procedures—and to upgrade their validation resources with MRM 2.0 firmly on the agenda.

By Horst Simon, The Risk Culture Builder. Bank regulators have been on a “capital charge”-path for a very long time. No capital charge can be a buffer for bad management of risk. History showed us that sometimes ALL the capital is not enough to save the bank from a risk event gone wrong.

Financial institutions’ reliance on information and communication technologies (ICT) for core operations brings immense opportunities in today’s digital world but also exposes banks, investment firms, insurers, and other financial entities to significant cyber threats and operational risks.

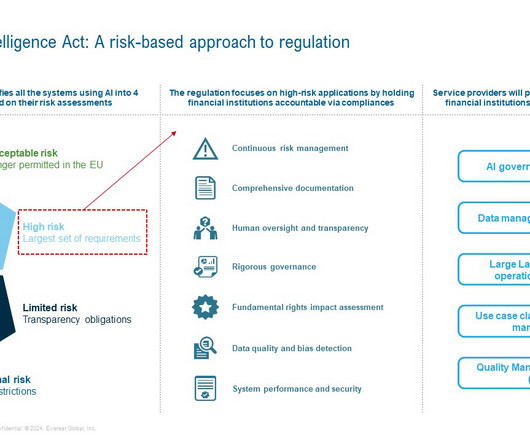

Next, they need to take inventory of existing AI assets like models, tools, and systems, classifying each into the four risk categories outlined by the Act. Crucially, a cross-functional team should be formed to oversee AI riskmanagement, drive compliance efforts, and execute mitigation plans across the organization.

SIG University Certified Third-Party RiskManagement Professional (C3PRMP) program graduate William Chanto Castro shares the tricks to overcoming the obstacles to meeting risk regulations and requirements. MAS, 2016, p.9). The C3PRMP program was created by Linda Tuck Chapman, an advisor, educator, author and expert.

As nonfinancial companies move from enterprise riskmanagement to a resilience-based approach, their experience in nonfinancial risk can provide a model for banks.

Views from Risk Professionals across the world. During the recording of “RiskManagers Getting Coffee” which can be found on YouTube HERE as well as on our website here , a few discussions came up with a recurring theme. One was the question of what makes a great riskmanager. Are there examples?

Sir Howard Davies discusses the ways regulations, interest rates, monetary policy, climate risk, and economic threats are affecting the resilience of the banking system.

Trust is the cornerstone on which the banking industry is built. When consumers lose trust in a bank’s ability to managerisk, the system stops working. Put simply, consumers trust banks to keep their money safe and return the money when requested. But there’s trust on the business side, too.

Poor riskmanagement practices, a questionable corporate culture, and a long series of scandals created an explosive mix that led to Credit Suisse’s collapse and consequent acquisition by rival UBS.

By Horst Simon, The Risk Culture Builder. Maybe the time has come to finally take the people side out of RiskManagement—let us change the Basle definition and say Operational Risk is just systems, processes and external events, that is anyway the perception that was followed by most in the world.

Any business loan or line of credit from a bank—brick-and-mortar or online—will carry more favorable terms if you have a decent business credit scor e. Lenders use your business credit score to determine how likely you are to repay your loan; the lower the score, the less attractive you are to a lender, especially banks.

UBS’ takeover of longtime rival Credit Suisse in a rushed, deeply discounted deal has reverberations across the banking and financial services (BFS) IT services market and on service providers. While the deal was made to prevent further meltdowns and stabilize the banking industry, risks of further blight spreading exist.

The impacts of AI on consumers, banks, nonbank financial institutions, and the financial system’s stability are all concerns to be investigated and potentially addressed by regulators. Hsu discussed the systemic risk implications of AI in banking and finance using a “tool or weapon” approach.

A top-leading bank, grappling with business and regulatory challenges, faced scrutiny after failing the Federal Reserve’s annual stress test. To bolster its capabilities and ensure compliance, the bank sought assistance from Perficient in delivering exceptional project and program management services to tackle their significant hurdles.

Global Business Services (GBS) organizations have a big opportunity to champion Environment, Social, and Governance (ESG) in banking and financial services (BFS) institutions. Capital market firms are embracing green underwriting, while asset and wealth managers are steadily moving toward ESG investing.

Additionally, the Supervisory Letter states that Board-supervised banking organizations should notify the Board prior to engaging in crypto-asset-related activities. The letter highlighted mandatory compliance with the following federal regulations: The Bank Holding Company Act. Financial risk. Legal risk.

Our bankingrisk and regulatory experts are excited to attend the upcoming XLoD Global event in New York on June 11th. The world’s leading financial institutions and regulators come together at XLoD to discuss the future of non-financial risk and control. What is XLoD Global?

Volumes have been written on the cause of the crisis the world is in, surveys have been done and many fingers are pointing in every direction—a couple of these are pointing straight at us, the Risk Professionals. It is time to renovate riskmanagement. The basic RiskManagement process cycle is one of those.

With this approach, we can strategize effectively, choosing paths that optimize financial gains, enhance social impact, or minimize risks. As financial intermediaries and riskmanagers, insurers have a unique ability to drive and support sustainable practices across different industries and communities.

While the world tried to recover from the slowdown, a new predicament posed as a challenge to the Banking industry – new-age Fintech firms. The steady and quick rise of Fintech firms in the world has shaken the presence and role of conventional banking. Banks collaborating and creating partnerships with Fintech is the way forward.

Watch the webinar, Transforming to Thrive: Building Winning Operating Models Amid Disruption Across Industries , to learn about trends impacting enterprises across industries, such as healthcare, life sciences, insurance, and banking and financial services?

Perficient is looking forward to joining this conversation with other financial services and payments experts at the upcoming Bank Automation Summit in Charlotte, North Carolina on March 2-3. With all this considered, key strategic topics like buy vs. build, risk, and operational readiness cannot be ignored.

This could exacerbate social inequality and unrest Impact on relations with China : This proposed move brings to light a crucial but often neglected concern regarding the continuity of the currency swap line between the Central Bank of the Argentine Republic (BCRA) and The People’s Bank of China (PBOC).

To help shed light on this matter, Perficient’s Financial Services Risk and Regulatory Center of Excellence (CoE) researched the topic extensively and discovered that the Office of the Comptroller of the Currency (OCC) has classified AI as an emerging risk to the banking industry.

The Russian military action in Ukraine has already significantly impacted thousands of services jobs in this region, but the potential reverberations to nearshore European countries and the larger global services industry could be far more damaging – making it essential to integrate geopolitical riskmanagement in your decision-making now.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content